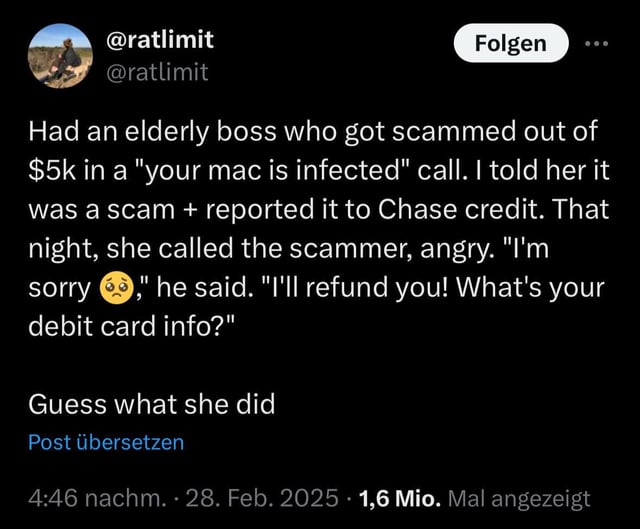

my dad almost fell for a chase/credit card phishing scam, luckily hes very poor and remember passwords. and asked us for advice we told him its a scam.

People tweeting stuff. We allow tweets from anyone.

RULES:

my dad almost fell for a chase/credit card phishing scam, luckily hes very poor and remember passwords. and asked us for advice we told him its a scam.

My elderly mother has her phone locked down so that you can't contact her unless you're in her contacts.

We need to rethink how we let random people contact other random people. The upside of letting random people call anybody isn't that large, and the downside is like billions of damages in scams and people losing their retirements.

I considered doing this, but then the Pixel phones started doing a much better job at just filtering out spam calls so it hasn't really been an issue.

No. What we need is freaking DNS for phone numbers. I don't get why this isn't a thing.

So you can actually register a bunch of numbers under the same name. If DoctorSocks.med calls, you know it is them regradless whether it's the front desk or what not.

If DrJoana@DoctorSocks.med calls, you know it's the number of that particular person.

In that way you can even establish curated lists. On a govermental, but also on a community level.

Hello it's me Bill Gates at rnicrosoft.com I will help you do the needful to fix your device.

See. This is exactly what would not happen.

Because granny's phone white lists the curated list from her government, her family, and, well, her individual phone. Guess what? Rnicrosoft.com is not on there. Plus, it would not work like real DNS. It's merely an anology.

So you can actually register a bunch of numbers under the same name

You can already do that with the ubiquitous vCard format.

Nope, this is not dynamic. If you call "DoctorSocks", you will reach them because it gets resolved for you. Not because you statically saved it on your device.

Does your mom not have any doctors?

She can simply save her doctors as contacts

The upside of letting random people call anybody isn’t that large

That really does depend on the person. My grandma can barely use email and doesn't know the difference between her Contacts app and Gmail, nor does she even understand how to add a contact. She'd just accidentally isolate herself from people without realizing, and would also never get any of the phone calls she gets from her bank, charities and organizations she works for, etc.

Those examples you mentioned aren't random people. They're people she knows and organizations that she associates with. I am suggesting that we rethink the system to specifically disallow randos.

People and organizations that:

That's why I'm saying it isn't for everyone. Sure, maybe you can find someone that does have a bank, medical providers, insurance providers, etc, that uses only one number for all phone-based communication and uses no third-parties, but that's not the norm, so for her, that would result in constantly missing bills, follow-up texts, fraud alerts, customer service callbacks, etc.

That's why the STIR/SHAKEN attestation was setup for VOIP.

It basically adds a layer of trust and verification that the person placing the call owns the number that is being used in the caller ID. It helps prevent random calls from being transmitted from random numbers, one of the reasons it's almost impossible to prevent scam calls right now.

But it's not enforced system wide, and we don't have legislature that is making a point to deal with these scam and junk calls.

Again, my suggestion was that we rethink the system, not that we keep the current system exactly as it is except that everybody locks down their cell phones. If we rethink the system, then those examples you thought of would be use cases for contacting people under the new system.

Have you ever had food (or package and furniture even) delivery where they need to call, or gotten a call from a pharmacy, or had to call a plumber, or lost a pet? There’s tons of reasons why people need to call a random person.

It makes sense to have the option to lock down a phone to just contacts, like for kids and the elderly, but not for everyone.

For me it's calls from medical professionals regarding my wife. There's no way to know ahead of time the entire list of numbers all of these organizations - each facility, each provider, each insurer, each pharmacy.

Definitely! And if you’re someone’s emergency contact, forget about it.

If you're hot, then giving randos your phone number is a recipe for stalkers.

Everyone should have multiple phone numbers, each with expiration dates that vary according to how long you expect to interact with them: 1 day for food delivery, 1 month for dating, 1 year for classmates, coworkers, or family. 10 years for close friends.

My ex fell for a "credit repair" scam over the phone. They said they'd charge a certain amount every month to her credit card and invest it in an account she could access in a year, and that it would look like she was paying off a debt.

She told them she didn't have a credit card, just a debit card. "That's fine," they said.

I asked her how she thought that would work and she said she didn't know.

I think this is what people are neglecting to point out. Sure scammers tend to target the elderly more but in all honesty, as per your example, all you need is one idiot.

My parents are in their 70s and have never fallen for this and they have been called a few times with these scams. my Dad will just tell them to fuck off and my Mom will essentially do the same but in a more polite British manner. Hell my mom is better at using her smartphone than I am, she just embraced that shit when it came out. My Dad has been using computers since the 70s and now runs Slackware of all distros on his PC. he loves it. So both are technologically savvy. I don't have to worry about them falling for scams. They've even gotten the scam call where someone claimed to be me or know me saying I was arrested and needed bail. they laughed them off because they KNEW I would never do something like that.

I asked her how she thought that would work and she said she didn’t know.

Fun fact, this is actually a real thing you can do, and the real ones aren't scams. (unless you consider paying a fee in exchange for quickly building solid credit history without spending money on goods a scam)

They're called Credit Builder Loans.

Essentially, you're not technically "putting money in an account", you're being given a loan at a future date, after you've made your payments. (basically just a reversed loan schedule) If you miss a payment due date, it hurts your credit just like missing a regular loan payment for money they already gave you.

Some charge interest (basically any given by for-profit companies/banks), some don't (mostly just the occasional credit union). They do exactly what the credit system is supposed to indicate, which is show that you can make payments consistently and on-time, regardless of if you got the money upfront or after.

Personally, I almost always would say secured credit cards and credit-building "debit" cards are a better option. (e.g. the Chime's and Step's of the world where your card limit is always your current balance and never more, except for overdrafts) If you look at a big credit builder loan provider like Self, you can see their plans result in you paying pretty large fees overall just to boost your credit score, like paying $600 in and getting $511 back on their cheapest plan. Ideally, you'd have a credit union that wouldn't charge a fee, but might just offer a low or no interest rate compared to investing it in a CD in exchange for them having to effectively hold that money for you instead of being able to offer it out for loans. (and even then, the term is fixed, so they can still loan it out as long as they know they'll get it paid back by the time your term ends)

no wait what? the bank is basically borrowing from me, and yet i can be charged an interest and be punished if i don't lend them money on time?

that, sir, sounds like a scam.

It's only a scam if they tell you one thing and charge you another. If the terms are laid out in plain English and everyone agrees to the terms, it's not a scam, no matter how bad those terms are for you.

yet i can be charged an interest and be punished if i don’t lend them money on time?

Yes, that's one of the reasons they work so well at quickly building up credit history for people with really bad credit to begin with. The credit bureaus see an actual loan, with actual interest, and actual required payments. If they didn't ding you for missing payments, then the credit bureaus wouldn't count it as a loan in the first place. There has to be some kind of pressure, consequence, and real-world stakes to missing payments to actually make it valid in their eyes, otherwise it's no different than a regular savings account you put money into whenever.

The entire point of it is to measure if you can be trusted to responsibly borrow or pay back money, they have to give conditions closer to actual loans to actually be considered in your credit score.

The trade is pretty simple, you give them some of your money, your credit score goes up. It might not be a good deal if you already have the ability to earn off a credit card, but these are mostly targeted at people who get rejected for any card they apply for. They're so low-risk for the company and so guaranteed that it's why they can offer them to basically anyone regardless of credit.

That said, I still would say secured cards are a better option, as nowadays there are cards where instead of it being like "give us a $200 payment and we'll give you a $400 credit limit with chances for increases later", it's "give us a $200 payment regardless of your credit score, and you can spend up to exactly $200, and maybe if your score goes up enough we'll give you the real deal".

The main problem with secured cards is that the way your credit score is calculated also calculates the % of your credit utilized. Higher is generally worse. So if you get a secured card, and the company offering it only allows you to start with $200, if you spend all $200, you'll actually get a smaller boost to your score than if you'd spent $50 out of the $200 and no more over the entire month, or spent $200 on credit builder loan payments, which counts as a full, outstanding debt, just one that you're regularly making payments on.

Again, this is why they are marketed to people looking to increase their score faster. You might spend more overall in interest, but you get a larger impact on your score than other options that factor in utilization, and they also tend to result in much larger increases over the same period for people that don't already have a line of credit, which is obviously good for... people who don't have access to credit and want to increase their score fast to get that access.

I wouldn't personally choose one, it makes no sense for my situation, but they are a good option if you are, generally speaking, unable to get other lines of credit, will spend close to the limit of a secured card, and/or need a higher score faster than you could otherwise slowly build it up.

I'm aware of these, and have done one myself. This isn't what they described, though, or at least not how she described it to me. Credit building loans are, well, loans, and as such have a specific "principal amount", pay off date, etc. This was supposed to just be an ongoing thing she could stop at any time and just have a fat chunk of change that's been growing with the stock market to stick in her pocket whenever she wanted.

In other words, a very obvious scam.

I think I know why that person doesn't have a credit card

I got scammed with a phishing email a few years back. I'm still pissed at myself. Motherfuckers got lucky. I had lost a credit card so I canceled it and got a replacement. I had several subscriptions on that card and I was going through changing my card info on them. I just so happened to get a scam "unable to process your payment" email for Netflix before I had changed the card info for it. I did what you never do. I clicked the link instead of going directly to Netflix and changed my payment info. Didn't notice anything was wrong until they bought a plane ticket with it. sigh

That's how those scam emails work, they know that some percentage of people will have just changed cards or something that day so they'll be inclined to believe the email.

Was good day. Their entire scam is base on them getting lucky, unfortunately. I've gotten hooked a couple time at first because it related to my life. My suspicious now triggered when I have to fill in too much detail to connect it to my actual life. The best lies use truths.

My sister once fell for a fake bank notification after she just set up her new phone's bank app.

Being old is not an excuse for being dumb.

I’m not talking about knowing stuff, but the inherent knowing-that-you-don’t-know.

Yep. Our parents always told us to not believe everything on the internet.

And now, they believe anything from some random shitbag overseas.

Do you not know how aging works?

There's a line between having full blown dementia and being entirely helpless with out help. And a random 65 year old just being fucking stupid cause they are "old" and stopped trying to think for themselves.

A LOT of elderly are still entirely of sound mind and just even attempting to think for themselves. Hell it is not even just the elderly. People let themselves go fucking retarded the moment they have to actually use their brain for anything outside their expertise or day to day tasks.

Its insanely frustrating to watch.

Yeah some times the scammers just get lucky or someone has a brain fart. It happens we all have off days.

But dear fuck do some people just never try.

No they aren't, even without dementia or other cognitive conditions, aging causes mental decline. This is widely researched and known.

Yes Cognitive decline is well researched and starts way earlier than your 60s, but its also an umbrella term for a lot of things.

Reaction and processing speed goes down starting from your mid 20s, short and long term memory gradually declines in your 30s and your vocabulary decreases from the mid 40s. But the ability for complex judgement that's important here shouldn't start declining until your 60s. If you are in your mid 60s and are completely helpless when it comes to technologie that's been around for 10+ years, you either are in the early stages of a cognitive condition like dementia or you are willfully ignorant cause you can't be bothered to learn.

There are a few other causes, like excessive lead exposure (which is especially common for Americans) and malnourishment during you development (often the case for developing nations), but at least the former can be classified as a neurological condition.

Idk I think everyone is dumb somewhere and I dont think people can generally identity where that is.

Exactly.

“You just won Beyoncé tickets!”

“Wow I didn’t even enter a contest, but ok!”

—A certain percentage of people off the street regardless of age

It kind of is. There is are a lot of people in the early stages of dementia or Alzheimer's who get easily confused and are aware that they can't trust their own memory. It's very easy to see how they could be talked into trusting someone they shouldn't.

You can wither use a credit card responsibly, or not have one. Credit card companies could probably do more here by making an "old person card" that can't be used to make online orders or phone orders, but until then, these people shouldn't be using credit cards with high limits.

I read this and for two seconds I thought "Oh, someone with some empathy and morals that shouldn't be doing this, how nice," then I remembered what species I'm a part of.