this post was submitted on 30 Dec 2024

1108 points (99.1% liked)

196

18890 readers

533 users here now

Be sure to follow the rule before you head out.

Rule: You must post before you leave.

Other rules

Behavior rules:

- No bigotry (transphobia, racism, etc…)

- No genocide denial

- No support for authoritarian behaviour (incl. Tankies)

- No namecalling

- Accounts from lemmygrad.ml, threads.net, or hexbear.net are held to higher standards

- Other things seen as cleary bad

Posting rules:

- No AI generated content (DALL-E etc…)

- No advertisements

- No gore / violence

- Mutual aid posts are not allowed

NSFW: NSFW content is permitted but it must be tagged and have content warnings. Anything that doesn't adhere to this will be removed. Content warnings should be added like: [penis], [explicit description of sex]. Non-sexualized breasts of any gender are not considered inappropriate and therefore do not need to be blurred/tagged.

If you have any questions, feel free to contact us on our matrix channel or email.

Other 196's:

founded 2 years ago

MODERATORS

you are viewing a single comment's thread

view the rest of the comments

view the rest of the comments

All kinds of low risk things go down occasionally. Think of the 2008 financial crash for example. On average, or over a long time, you are very likely to make gains. But that’s not nevessarily true for shorter periods like 10 years even if you invest in low risk assets.

Edit: I also invested some of my student loans in Finland. Or officially, my other income that was freed up due to the loan ¯_(ツ)_/¯

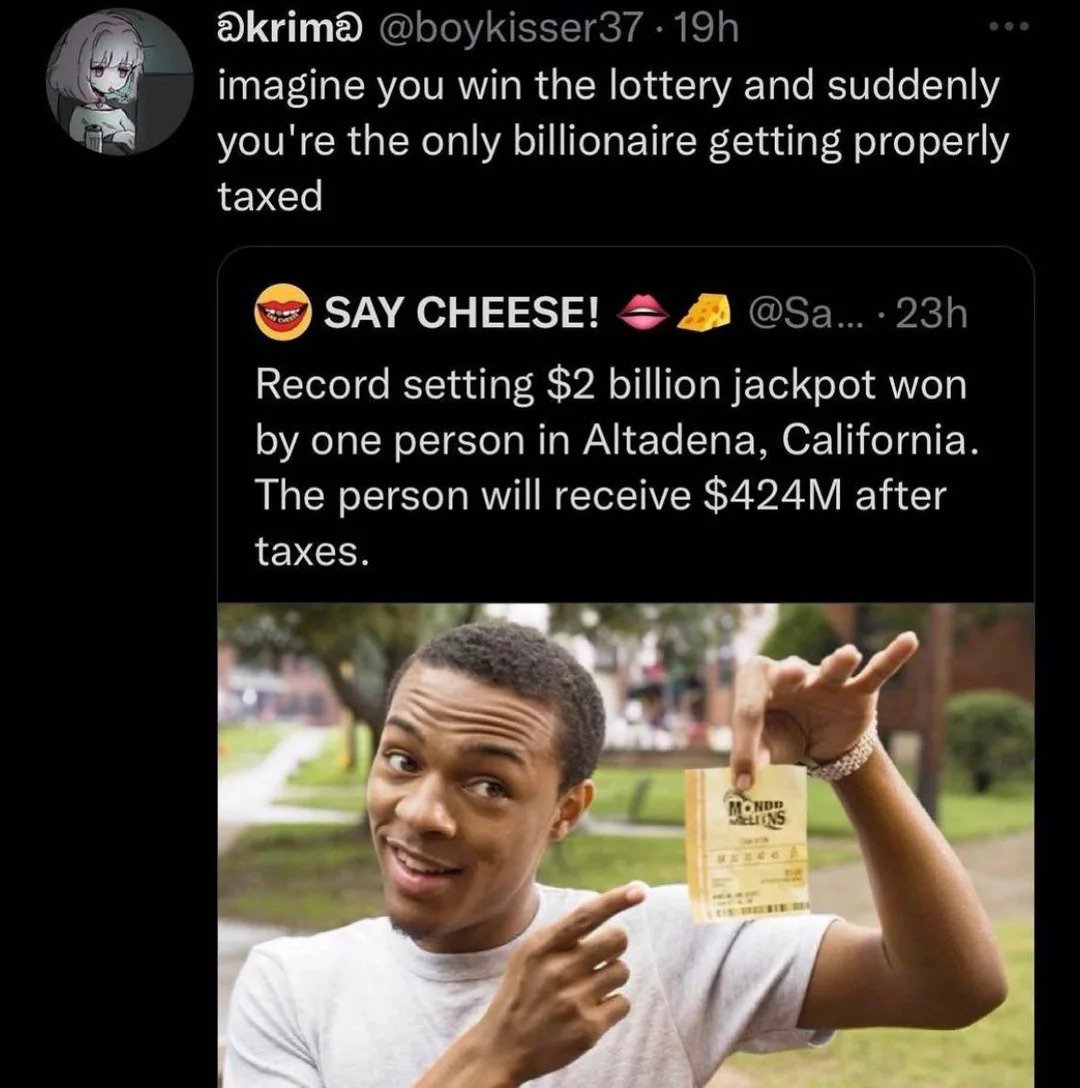

well he made the profit in like 2 years lol.

Also there's at least one bank here that specifically only has savings accounts, with pretty decent interest (like 2.7%) and free withdrawals at any time. And because it's sweden the state will protect any money you deposit under like $100k per person.

For the last year or so getting a 5% (1-3 yr) CD was not unheard of, so literally leaving it in a bank account is better than the annuity option by the above poster's math.

I don't think you quite understand what I mean. You can't extrapolate from the last 3 years. What you can extrapolate from is longer periods of time, where we occasionally see assets going generally down for some time. So you have maybe 90% chance of your stock portfolio going up in the next 5 or 10 years, and 10% chance of it going down (rough numbers but the point holds).

So you can end up in a situation where you lose money, but it's unlikely. If you are very risk averse, you would prefer a 0% increase over these odds.