this post was submitted on 14 Jul 2026

752 points (98.1% liked)

Work Reform

16866 readers

1182 users here now

A place to discuss positive changes that can make work more equitable, and to vent about current practices. We are NOT against work; we just want the fruits of our labor to be recognized better.

Our Philosophies:

- All workers must be paid a living wage for their labor.

- Income inequality is the main cause of lower living standards.

- Workers must join together and fight back for what is rightfully theirs.

- We must not be divided and conquered. Workers gain the most when they focus on unifying issues.

Our Goals

- Higher wages for underpaid workers.

- Better worker representation, including but not limited to unions.

- Better and fewer working hours.

- Stimulating a massive wave of worker organizing in the United States and beyond.

- Organizing and supporting political causes and campaigns that put workers first.

founded 3 years ago

MODERATORS

you are viewing a single comment's thread

view the rest of the comments

view the rest of the comments

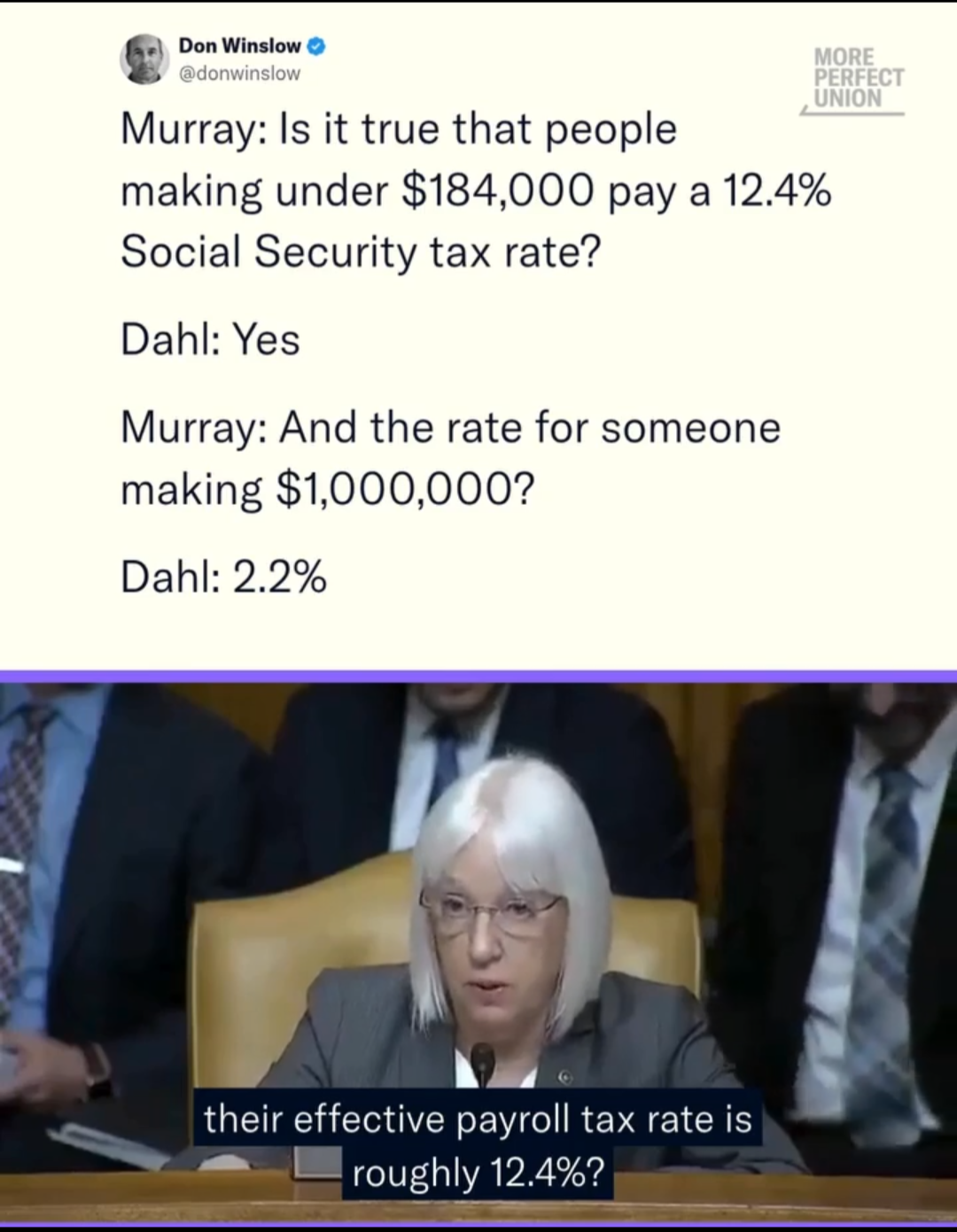

The reason this works out that way is because there is a wage base for the social security tax. If you don’t make more than that base then you pay that tax all year long. If you’re making 1m then you pay that tax for like the first two months and then nothing afterwards. The solution to this is just removing the wage base. If you make 1m you should pay the same percentage as everybody else on all your earnings. Magically the social security system will be overfunded.

With Social Security, the amount you get out is directly related to the amount you pay in. So if the cap is increased, yes, social security will get more income, but they'll also need to start paying out a whole ton more.

It's more of a forced savings/investment account than a wealth redistribution scheme. There is some redistribution happening, but not as much as most people think.

It's a progressive payout though. SSA pays out 90 percent of average monthly income over 35 years (approximate based on their formula. AIME) below the first "bend" at about 1200 dollars per month, 32 percent between the first and second bend, and 15% above the second bend. So SSA would get 10.6 percent of every new dollar that used to be above the cap, while that dollar would increase the person's benefit by their marginal rate (likely 32 or 15 for a high earner) divided by 420 months (you could assume the person will have a 35 year retirement to cancel out the two sides of the equation). Turning 10.6 percent into 15-32% (and most of the uncapped money would be likely to fall in the 15% if I had to guess) shouldn't be a hard thing to do for SSA with extra funds to spare when you consider that the average retiree won't live for a 35 year retirement and that there are 35 years of gains to capture between money in time vs money out time